Regression Review

Linear Regression

- Correlation and regression are similar

- Correlation determines the standardized relationship between X and Y

- Linear regression = 1 DV and 1 IV, where the relationship is a straight line

- Linear regression determines how X predicts Y

- Multiple (linear) regression = 1 DV and 2 + IV (also straight lines)

- Multiple regression determines how X, Z, and etc, predict Y

Modern Regression Equation

- \(Y=B_{YX}X + B_0 + e\)

- \(Y\) = predict value

- \(B_{YX}\) = slope [also can be written as \(B_{1}\) when we get to MR]

- \(B_{0}\) = intercept

- \(e\) = error term (observed - predicted). Also called the residual.

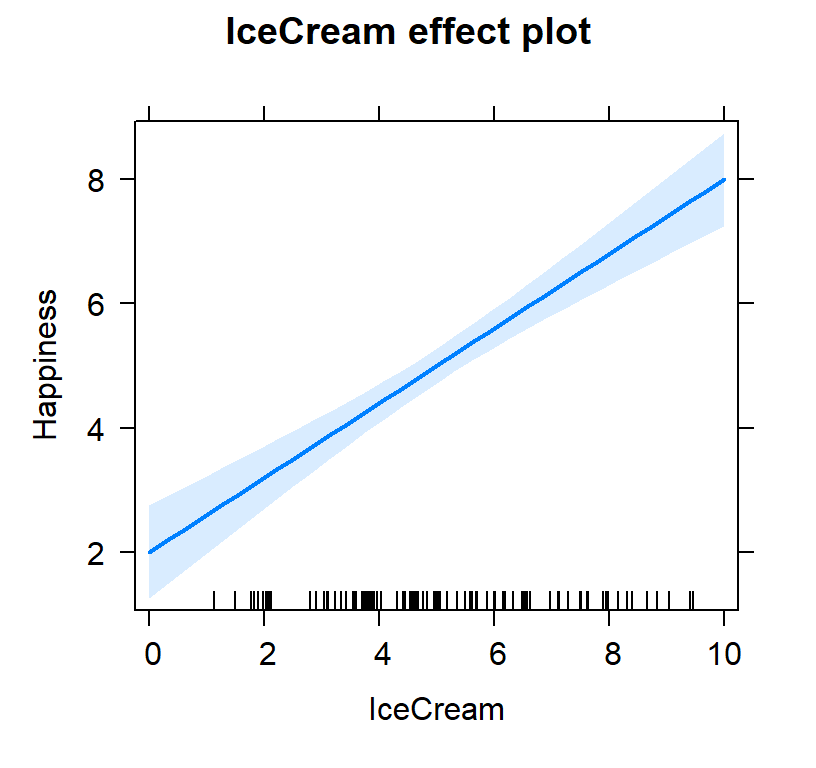

Ice cream example

- We are going to predict happiness scores from the number of spoons

of ice cream.

- Specify the model with the lm function.

set.seed(666)

library(car) #graph data

# 100 people

n <- 100

# Uniform distrobution of Ice Cream scoops

X <- runif(n, 0, 10)

# Slope

Byx<-.6

#intercept

B0 <- 4

# noise

e <- rnorm(n, sd=1.5)

# Our equation to create Y

Y = Byx*X + B0 + e

#Convert them to a "Data.Frame", which is like SPSS data window

#Built our data frame

IceCreamStudy<-data.frame(Happiness=Y,IceCream=X)

#Extract vectors

IceCream<-IceCreamStudy$IceCream

Happiness<-IceCreamStudy$Happiness

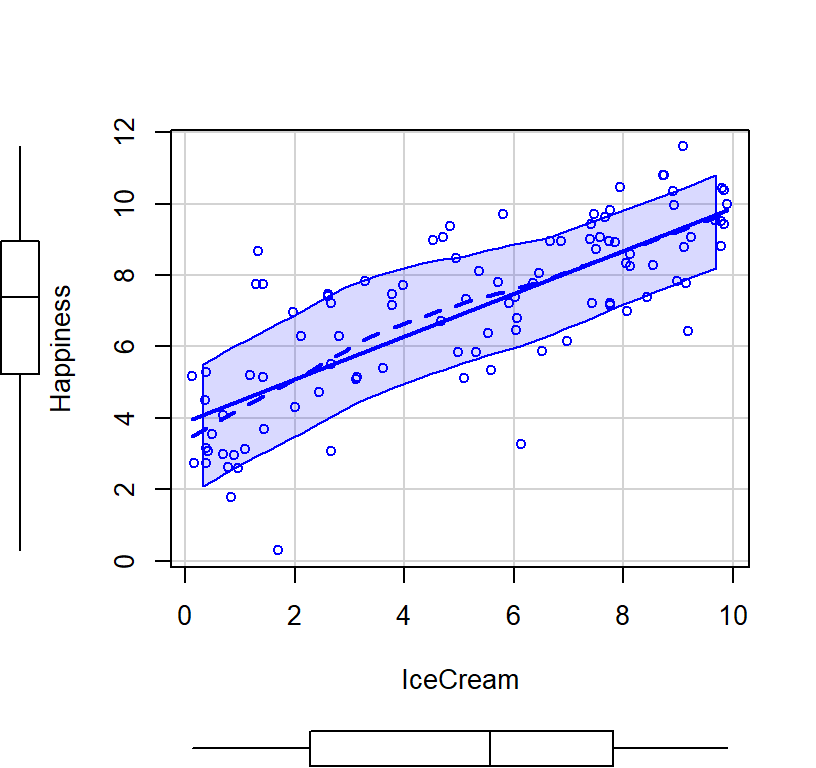

scatterplot(Happiness~IceCream, smoother=FALSE)

Happy.Model.1<-lm(Happiness~IceCream,data = IceCreamStudy)library(stargazer) # Make APA like tables

stargazer(Happy.Model.1,type="html",

intercept.bottom = FALSE,

single.row=TRUE,

star.cutoffs=c(.05,.01,.001),

notes.append = FALSE,

header=FALSE)| Dependent variable: | |

| Happiness | |

| Constant | 3.895*** (0.301) |

| IceCream | 0.600*** (0.050) |

| Observations | 100 |

| R2 | 0.595 |

| Adjusted R2 | 0.591 |

| Residual Std. Error | 1.551 (df = 98) |

| F Statistic | 144.046*** (df = 1; 98) |

| Note: | p<0.05; p<0.01; p<0.001 |

Intercept

- 3.895 is where the line hit the y-intercept (when happiness = 0).

Slope

- 0.6 is the rise over run

- for each 0.6 change in ice cream value, there is a corresponding change in happiness!

- so we can predict happiness from ice cream score:

(0.6 * 5 spoons of ice cream + baseline happiness intercept: 3.895) = 6.895

- This is your predicted happiness score if you had 5 spoons of ice cream

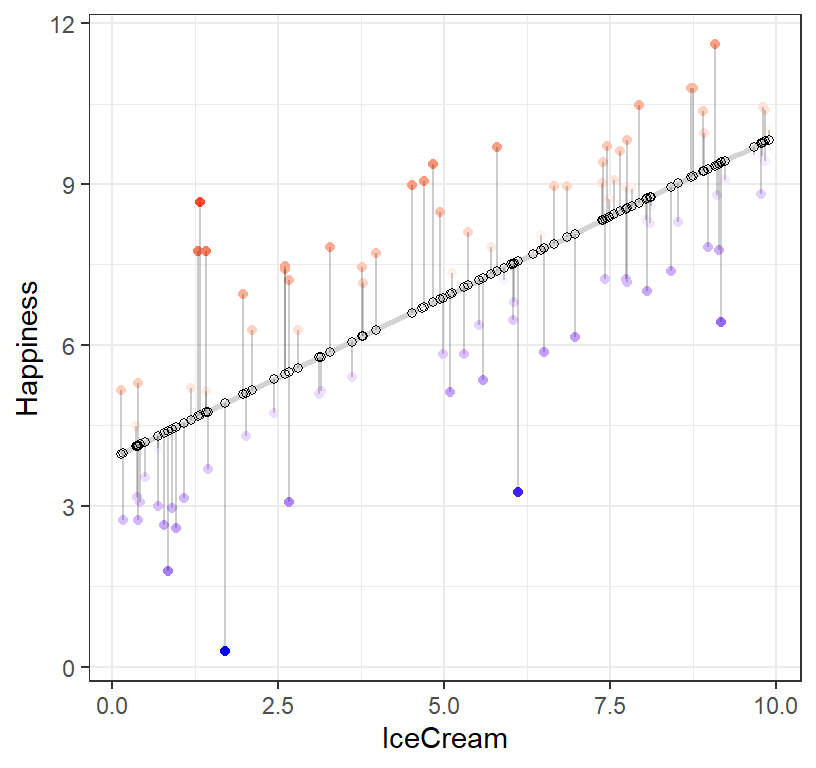

Error for this prediction?

R will actually do all the prediction for us for each value of ice cream residuals = observed - predicted

- Red dots = observed above predictor line

- Blue dots = observed below predictor line

- the stronger the color, the more an impact that point has in pulling the line in its direction

- Hollow dots = predicted

- The gray lines are the distance between observed and predicted values!

What should the mean of the residuals equal?

# Save the predicted values with our real data

IceCreamStudy$predicted <- predict(Happy.Model.1)

# Save the residual values

IceCreamStudy$residuals <- residuals(Happy.Model.1)

library(ggplot2) #Fancy pants plotting system

ggplot(data = IceCreamStudy, aes(x = IceCream, y = Happiness)) +

geom_smooth(method = "lm", se = FALSE, color = "lightgrey") + # Plot regression slope

geom_point(aes(color = residuals)) + # Color mapped here

scale_color_gradient2(low = "blue", mid = "white", high = "red") + # Colors to use here

guides(color = FALSE) +

geom_segment(aes(xend = IceCream, yend = predicted), alpha = .2) + # alpha to fade lines

geom_point(aes(y = predicted), shape = 1) +

theme_bw() # Add theme for cleaner look

Ordinary least squares (OLS)

- Linear regression finds the best fit line by trying to minimize the sum of the squares of the differences between the observed responses those predicted by the line.

- OLS computationally simple to get the slope value, but is actually inaccurate.

- OLS cannot “fail” to find an answer

\[B_{YX}=\frac{\sum{XY}-\frac{1}{n}\sum{X}\sum{Y}}{\sum{x^2}-\frac{1}{n}\sum{x}^2} = \frac{Cov_{XY}}{var_x}\]

- Mixed-effects models use (ML, REML) to fit. These are more accurate, but can fail (we will return to ML/REML soon).

SE on the terms in the models

- How good is the fit?

- Residual Standard error = \(\sqrt\frac{\sum{e^2}}{n-2}\)

- in R langauge:

n=length(IceCreamStudy$residuals)

RSE = sqrt(sum(IceCreamStudy$residuals^2) / (n-2))- So our error on the prediction is 1.5505018 happiness points based on our model.

SE on the Intercept

- Intercept Standard error = \(RSE\sqrt {\frac{1}{n}+\frac{M_x^2}{(n-1)var_x}}\)

- in R langauge:

ISE = RSE*(sqrt( (1 / n) + (mean(IceCreamStudy$IceCream))^2

/ ((n - 1)*var(IceCreamStudy$IceCream))))- our SE on the intecept is 0.3012578

SE on the Slope

- Intercept Standard error = \(\frac{sd_y}{sd_x}\sqrt{\frac{1 - r_YX^2}{n-2}}\)

- in R language:

#lets extract the r2 from the model

r2.model<-summary(Happy.Model.1)$r.squared

SSE = sd(IceCreamStudy$Happiness)/sd(IceCreamStudy$IceCream) *

sqrt((1- r2.model)/ (n - 2))- SE on the slope is 0.0499665

t-tests on slope and intercept and \(r^2\) value

- Values are tested against 0, so its all one sample t-tests

- slope: \(t = \frac{B_{YX} - H_0}{SE_{B_{YX}}}\)

- intercept: \(t = \frac{B_{0} - H_0}{SE_{B_{0}}}\)

\(r^2\) is a little different as its a correlation value

- correlations are not normally distributed

- Fisher created a coversion for r to make it a z (called Fishers’ \(r\) to \(Z\))

- \(r^2\): \(t = \frac{r_{XY}\sqrt{n-2}-H_0}{\sqrt{1-r_{XY}^2}}\) , where \(df = n - 2\)

- its often given for as an F value, remember \(t = F^2\)

#intercept

t.I= Happy.Model.1$coefficients[1]/ISE

#Slope

t.S= Happy.Model.1$coefficients[2]/SSE

# For r-squared

t.r2xy = r2.model^.5*sqrt(n-2)/sqrt(1-r2.model)

F.r2xy = t.r2xy^2- Intercept t = 12.929604

- Slope t = 12.0018969

- \(R^2\) F-test = 144.0455294

- Note: We are testing null hypothesis value for slope, i.e., null = 0. But it’s a terrible guess. Everything correlates with everything, so it’s important to keep this in mind moving forward.

Regression in ANOVA format

- You can also report the results of all the predictors (if you have multiple) in ANOVA style format (F-test we calculated above on \(R^2\))

- This is useful in multiple regression as it tell your if your overall set of predictors is significant

anova(Happy.Model.1)## Analysis of Variance Table

##

## Response: Happiness

## Df Sum Sq Mean Sq F value Pr(>F)

## IceCream 1 346.29 346.29 144.05 < 2.2e-16 ***

## Residuals 98 235.60 2.40

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Multiple Regresion

With No Redundancy

- Predictors do not correlate with each other

- Ice cream spoons (X1)

- Brownies squares (X2)

- Happiness score (Y)

- We will assume ice cream and brownies are unqiue predictors of happiness

- Note: The simulations are based on multivariate functions now so we can control the relationships between the variables very carefully.

- We will set a mean for each at 5 and create a covariance matrix between the variables

\[ \mathbf{Cov} = \sigma^2\left[\begin{array} {rrr} 1 & 0 & .6 \\ 0 & 1 & .4 \\ .6 & .4 & 1 \end{array}\right] \] where, \(\sigma^2 = 4\)

- tow column order

- Ice cream, 2. Brownines, 3. Happiness

- Simulation below:

library(MASS) # use multivariate norm function to better control relationships

py1 =.6 #Cor between X1 (ice cream) and happiness

py2 =.4 #Cor between X2 (Brownies) and happiness

p12 = 0 #Cor between X1 (ice cream) and X2 (Brownies)

Means.X1X2Y<- c(5,5,5) #set the means of X and Y variables

CovMatrix.X1X2Y <- matrix(c(1,p12,py1,

p12,1,py2,

py1,py2,1),3,3)*4 # creates the covariate matrix

#build the correlated variables. Note: empirical=TRUE means make the correlation EXACTLY r.

# if we say empirical=FALSE, the correlation would be normally distributed around r

set.seed(666)

CorrDataT<-mvrnorm(n=100, mu=Means.X1X2Y,Sigma=CovMatrix.X1X2Y, empirical=TRUE)

#Covert them to a "Data.Frame", which is like SPSS data window

CorrDataT<-as.data.frame(CorrDataT)

#lets add our labels to the vectors we created

colnames(CorrDataT) <- c("IceCream","Brownies","Happiness")

CorrDataT$Happiness<-CorrDataT$Happiness

# Correlations

ry1<-cor(CorrDataT$Happiness,CorrDataT$IceCream)

ry2<-cor(CorrDataT$Happiness,CorrDataT$Brownies)

r12<-cor(CorrDataT$Brownies,CorrDataT$IceCream)- Run model and report results

###############Model 1

Ice.Model<-lm(Happiness~ IceCream, data = CorrDataT)

###############Model 2

Ice.Brown.Model<-lm(Happiness~ IceCream+Brownies, data = CorrDataT)

stargazer(Ice.Model,Ice.Brown.Model,type="html",

column.labels = c("Model 1", "Model 2"),

intercept.bottom = FALSE,

single.row=TRUE,

star.cutoffs=c(.05,.01,.001),

notes.append = FALSE,

header=FALSE)| Dependent variable: | ||

| Happiness | ||

| Model 1 | Model 2 | |

| (1) | (2) | |

| Constant | 2.000*** (0.435) | -0.000 (0.517) |

| IceCream | 0.600*** (0.081) | 0.600*** (0.070) |

| Brownies | 0.400*** (0.070) | |

| Observations | 100 | 100 |

| R2 | 0.360 | 0.520 |

| Adjusted R2 | 0.353 | 0.510 |

| Residual Std. Error | 1.608 (df = 98) | 1.400 (df = 97) |

| F Statistic | 55.125*** (df = 1; 98) | 52.542*** (df = 2; 97) |

| Note: | p<0.05; p<0.01; p<0.001 | |

#packages we will need to plot our results

library(effects)#plot individual effects

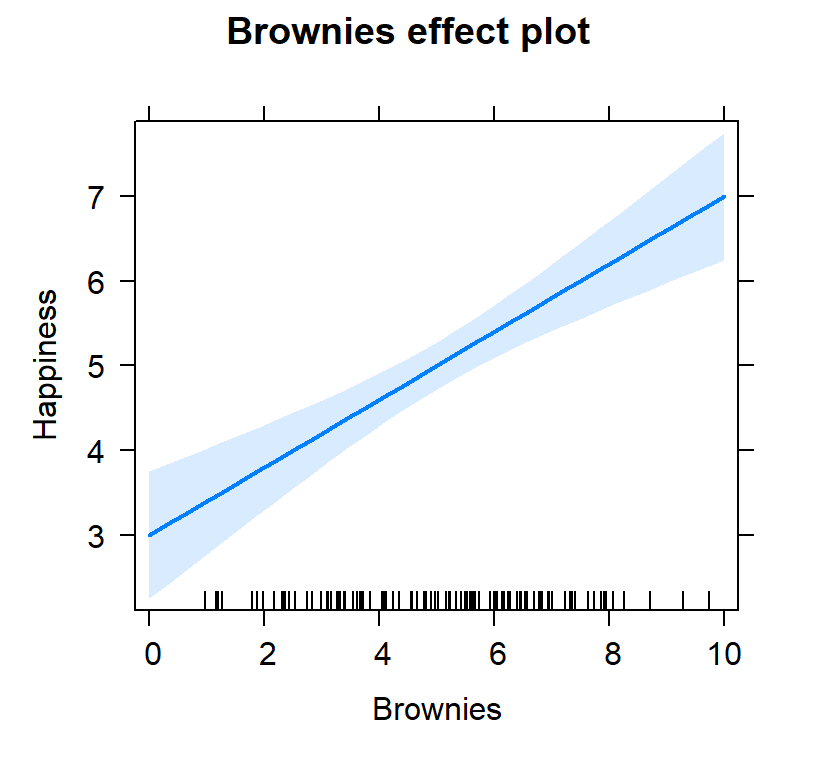

Ice.Brown.Model.Plot <- allEffects(Ice.Brown.Model,

xlevels=list(IceCream=seq(0, 10, 1),

Brownies=seq(0, 10, 1)))

plot(Ice.Brown.Model.Plot,

'IceCream', ylab="Happiness")

plot(Ice.Brown.Model.Plot,

'Brownies', ylab="Happiness")

#plot both effects

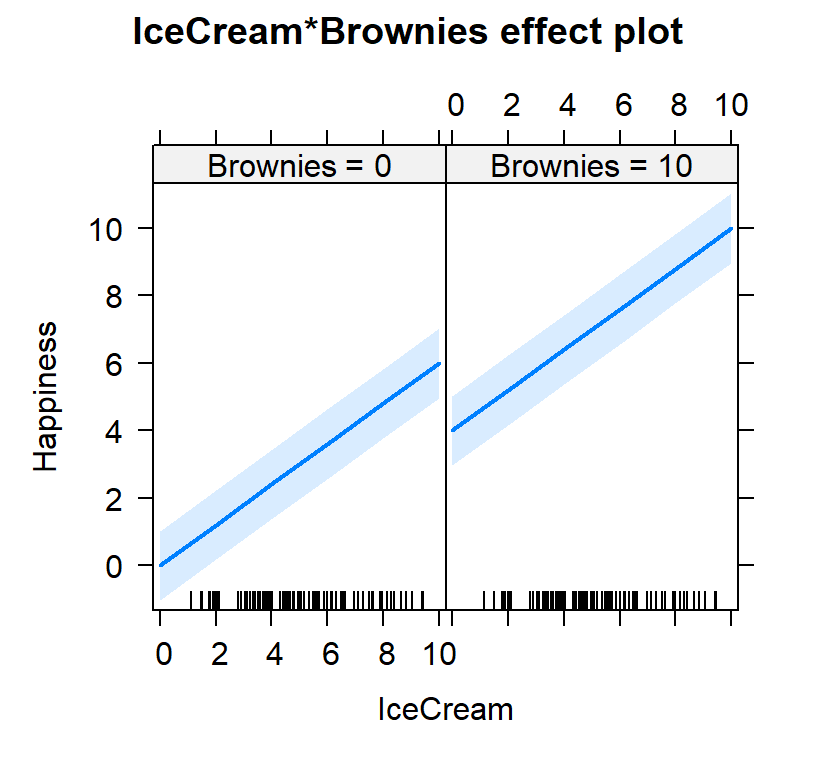

Ice.Brown.Model.Plot2<-Effect(c("IceCream", "Brownies"),

Ice.Brown.Model,

xlevels=list(IceCream=c(0, 10),

Brownies=c(0,10)))

plot(Ice.Brown.Model.Plot2)

Intercept

- Why did my intercept change?

- Intercept is the 0 point for ice cream and 0 brownies.

- See the figure above for the new intercept when both predictors are in the model

- We can fix the problem by centering our predictors [scale function]

# Center variables (if you said scale = TRUE it would zscore the predictors)

CorrDataT$IceCream.C<-scale(CorrDataT$IceCream, scale=FALSE, center=TRUE)[,]

CorrDataT$Brownies.C<-scale(CorrDataT$Brownies, scale=FALSE, center=TRUE)[,]

###############Model 1 Centered

Ice.Model.C<-lm(Happiness~ IceCream.C, data = CorrDataT)

###############Model C Centered

Ice.Brown.Model.C<-lm(Happiness~ IceCream.C+Brownies.C, data = CorrDataT)stargazer(Ice.Model.C,Ice.Brown.Model.C,type="html",

column.labels = c("Model 1", "Model 2"),

intercept.bottom = FALSE,

single.row=TRUE,

star.cutoffs=c(.05,.01,.001),

notes.append = FALSE,

header=FALSE)| Dependent variable: | ||

| Happiness | ||

| Model 1 | Model 2 | |

| (1) | (2) | |

| Constant | 5.000*** (0.161) | 5.000*** (0.140) |

| IceCream.C | 0.600*** (0.081) | 0.600*** (0.070) |

| Brownies.C | 0.400*** (0.070) | |

| Observations | 100 | 100 |

| R2 | 0.360 | 0.520 |

| Adjusted R2 | 0.353 | 0.510 |

| Residual Std. Error | 1.608 (df = 98) | 1.400 (df = 97) |

| F Statistic | 55.125*** (df = 1; 98) | 52.542*** (df = 2; 97) |

| Note: | p<0.05; p<0.01; p<0.001 | |

- The table now matches our simulation perfectly

Multiple R

- We use the capital letter, \(R\), now cause we have multiple X variables

- \(R_{Y.12} = \sqrt{\frac{r_{Y1}^2 + r_{Y2}^2 - 2r_{Y1} r_{Y2} r_{12}} {1 - r_{12}^2}}\)

- \(R_{Y.12} =\) 0.7211103

- if we square that value, 0.52, we get the Multiple \(R^2\)

- or the total variance explained by these variables on happiness

Estimating population R-squared

- \(\rho^2\) is estimated by multiple \(R^2\)

- Problem: in small samples correlations are unstable (and inflated)

- Also, as we add predictors, \(R^2\) gets inflated

- So we use an adjusted multiple \(R^2\)

- Adjusted \(R^2 = 1 - 1- R_Y^2 \frac{n-1}{n-k-1}\)

Partial Redundancy

- Regressions/correlations with more than 2 variables often presentes

a new challenge

- What if a third variable (X2) actually explains the relationship between X1 and Y?

- We need to find a way to figure out how X2 might relate to X1 and Y!

- In short: What happens if the predictors did correlate with each other?

- New question: How much does ice cream and brownies predict/explain happiness scores given ice cream and bronwies correlate with each other?

\[ \mathbf{Cov} = \sigma^2\left[\begin{array} {rrr} 1 & .3 & .6 \\ .3 & 1 & .4 \\ .6 & .4 & 1 \end{array}\right] \] where, \(\sigma^2 = 4\)

- Row/column order

- Ice cream, 2. Brownines, 3. Happiness

- Simulation below:

library(MASS) #create data

py1 =.6 #Cor between X1 (ice cream) and happiness

py2 =.4 #Cor between X2 (Brownies) and happiness

p12= .3 #Cor between X1 (ice cream) and X2 (Brownies)

Means.X1X2Y<- c(5,5,5) #set the means of X and Y variables

CovMatrix.X1X2Y <- matrix(c(1,p12,py1,

p12,1,py2,

py1,py2,1),3,3)*4 # creates the covariate matrix

set.seed(42)

CorrDataT2<-mvrnorm(n=100, mu=Means.X1X2Y,Sigma=CovMatrix.X1X2Y, empirical=TRUE)

#Convert them to a "Data.Frame", which is like SPSS data window

CorrDataT2<-as.data.frame(CorrDataT2)

#lets add our labels to the vectors we created

colnames(CorrDataT2) <- c("IceCream","Brownies","Happiness")

# Pearson Correlations

ry1<-cor(CorrDataT2$Happiness,CorrDataT2$IceCream)

ry2<-cor(CorrDataT2$Happiness,CorrDataT2$Brownies)

r12<-cor(CorrDataT2$Brownies,CorrDataT2$IceCream)What the problem?

- Ice Cream can explain happiness, \(r^2 =\) 0.36

- Brownies can explain happiness, \(r^2 =\) 0.16

- But how we do know whether Ice Cream and Brownies are explaining the same variance? Brownies and Ice Cream explain each other a little, \(r^2 =\) 0.09

Impacts on regression

- The slope for Ice cream should be B1 = 0.6

- The slope for Brownies should be B2 = 0.4

- but we know from the simulation that Ice cream and Brownies correlate, \(r =\) 0.3

# Center variables (if you said scale = TRUE it would zscore the predictors)

CorrDataT2$IceCream.C<-scale(CorrDataT2$IceCream, scale=FALSE, center=TRUE)[,]

CorrDataT2$Brownies.C<-scale(CorrDataT2$Brownies, scale=FALSE, center=TRUE)[,]

###############Model 1 Centered

Ice.Model.C2<-lm(Happiness~ IceCream.C, data = CorrDataT2)

###############Model C Centered

Ice.Brown.Model.C2<-lm(Happiness~ IceCream.C+Brownies.C, data = CorrDataT2)stargazer(Ice.Model.C2,Ice.Brown.Model.C2,type="html",

column.labels = c("Model 1", "Model 2"),

intercept.bottom = FALSE, single.row=TRUE,

star.cutoffs=c(.05,.01,.001), notes.append = FALSE,

header=FALSE)| Dependent variable: | ||

| Happiness | ||

| Model 1 | Model 2 | |

| (1) | (2) | |

| Constant | 5.000*** (0.161) | 5.000*** (0.155) |

| IceCream.C | 0.600*** (0.081) | 0.527*** (0.082) |

| Brownies.C | 0.242** (0.082) | |

| Observations | 100 | 100 |

| R2 | 0.360 | 0.413 |

| Adjusted R2 | 0.353 | 0.401 |

| Residual Std. Error | 1.608 (df = 98) | 1.548 (df = 97) |

| F Statistic | 55.125*** (df = 1; 98) | 34.150*** (df = 2; 97) |

| Note: | p<0.05; p<0.01; p<0.001 | |

- The slopes do not match the simulation slopes

Semipartial (part) correlation

- We need to define to contribution of each X variable on Y

- Semipartial (also called part) is one of two methods, the other is called partial

- is called semi, cause it removes the effect of one IV relative to the other without removing the relationship to Y

- Semipartial correlations indicate the “unique” contribution of an independent variable.

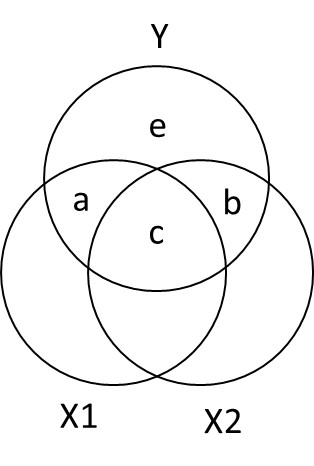

Ballantine for X1, X2, and Y

- \(R_{Y.12}^2 = a + b + c\)

- \(sr_1^2: a = R_{Y.12}^2 - r_{Y2}^2\)

- \(sr_2^2:b = R_{Y.12}^2 - r_{Y1}^2\)

Calcuation

- Calcuate unique varience

R2y.12<-sqrt((ry1^2+ry2^2 - (2*ry1*ry2*r12))/(1-r12^2))^2

a = R2y.12 -ry2^2

b = R2y.12 -ry1^2 - in other words,

- In total we explained, 0.4131868 of the happiness ratings (matches our \(R^2\) values from the regression table above)

- ice cream uniquely explained, 0.2531868 of happiness ratings

- brownies uniquely explained, 0.0531868 of happiness ratings

- We should not solve for c cause it can be negative (in some cases)

Seeing control in action in regression

- Another way to understand it:

- What if you want to know about happiness and how ice cream uniquely explains it? [controling the effect of brownies on ice cream]

- We can remove affect of brownies on ice cream by extracting the residuals lm(X1~X2)

- Remember the residuals are the left over (after extracting what was explainable)

- Next we can correlate happiness with the residualized ice cream.

#control for brownies

CorrDataT2$Ice.control.Brownies<-residuals(lm(IceCream~Brownies, CorrDataT2))

Sr1.alt<-cor(CorrDataT2$Ice.control.Brownies,CorrDataT2$Happiness)If we sqaure the correlation value we got 0.5031767, it becomes 0.2531868 which matches our \(a\) from the analysis above.

- We can repeat this analysis but changing our control to find \(b\).

#control for ice cream

CorrDataT2$Brownies.control.Ice<-residuals(lm(Brownies~IceCream, CorrDataT2))

Sr2.alt<-cor(CorrDataT2$Happiness,CorrDataT2$Brownies.control.Ice)If we sqaure the correlation value we got 0.2306227, it becomes 0.0531868 which matches our \(b\) from the analysis above.

- Thus in regression when we have more than one predictors they are controling for each other!

Relative importance

- There is a package that will do most of tht work for us

- The function calc.relimp in relaimpo has

lots of paramaters

- first would be if we entered them one at time

- last matches are semipartialed results (but order can matter)

library(relaimpo)

crlm <- calc.relimp(Ice.Brown.Model.C2,

type = c("first","last"), rela = FALSE )

crlm## Response variable: Happiness

## Total response variance: 4

## Analysis based on 100 observations

##

## 2 Regressors:

## IceCream.C Brownies.C

## Proportion of variance explained by model: 41.32%

## Metrics are not normalized (rela=FALSE).

##

## Relative importance metrics:

##

## last first

## IceCream.C 0.25318681 0.36

## Brownies.C 0.05318681 0.16Full Redundancy (Spurious models)

- when, \(r_{Y2} \approx r_{Y1}r_{12}\)

- X1 is confounded in X2

- X1 and X2 are completely redundant

\[ \mathbf{Cov} = \sigma^2\left[\begin{array} {rrr} 1 & .99 & .6 \\ .99 & 1 & .6 \\ .6 & .6 & 1 \end{array}\right] \] where, \(\sigma^2 = 4\)

- Row/column order

- Oreos, 2. Cookies, 3. Happiness

- Simulation below:

library(MASS) # use multivariate norm function to better control relationships

I.py1 =.6 #Cor between X1 Oreos and happiness

I.py2 =.6 #Cor between X2 Cookies and happiness

I.p12 = .99 #Cor between X1 Oreos and X2 Cookies

I.Means.X1X2Y<- c(0,0,0) #set the means of X and Y variables

I.CovMatrix.X1X2Y <- matrix(c(1,I.p12,I.py1,

I.p12,1,I.py2,

I.py1,I.py2,1),3,3)*4 # creates the covariate matrix

set.seed(42)

IData<-mvrnorm(n=100, mu=I.Means.X1X2Y,Sigma=I.CovMatrix.X1X2Y, empirical=TRUE)

#Covert them to a "Data.Frame", which is like SPSS data window

IData<-as.data.frame(IData)

#lets add our labels to the vectors we created

colnames(IData) <- c("Oreos","Cookies","Happiness")

###############Model 1

Oreos.model<-lm(Happiness~ Oreos, data = IData)

###############Model 2

Cookies.model<-lm(Happiness~ Cookies, data = IData)

###############Model 3

Oreos.cookies.model<-lm(Happiness~ Oreos+Cookies, data = IData)stargazer(Oreos.model,Cookies.model,Oreos.cookies.model,type="html",

column.labels = c("Oreos", "Cookies","Oreos+Cookies" ),

intercept.bottom = FALSE,

single.row=TRUE,

star.cutoffs=c(.05,.01,.001),

notes.append = FALSE,

header=FALSE)| Dependent variable: | |||

| Happiness | |||

| Oreos | Cookies | Oreos+Cookies | |

| (1) | (2) | (3) | |

| Constant | -0.000 (0.161) | -0.000 (0.161) | -0.000 (0.161) |

| Oreos | 0.600*** (0.081) | 0.302 (0.575) | |

| Cookies | 0.600*** (0.081) | 0.302 (0.575) | |

| Observations | 100 | 100 | 100 |

| R2 | 0.360 | 0.360 | 0.362 |

| Adjusted R2 | 0.353 | 0.353 | 0.349 |

| Residual Std. Error | 1.608 (df = 98) | 1.608 (df = 98) | 1.614 (df = 97) |

| F Statistic | 55.125*** (df = 1; 98) | 55.125*** (df = 1; 98) | 27.496*** (df = 2; 97) |

| Note: | p<0.05; p<0.01; p<0.001 | ||

Suppression

- Suppression is a strange case where the IV -> DV relationship is hidden (suppressed) by another variable

- Tax cuts cause growth, tax cuts cause inflation. Tax cuts alone might look +, but add in inflation and now tax cuts could make cause the growth to look different

- Or the the suppressor variable can cause a flip in the sign of the relationship

- Here is an example where the effect was hidden:

sup.py1 = 2.5 #Covar between tax cuts and growth

sup.py2 = -5.5 #Covar between inflation and growth

sup.p12 = 4 #Covar between tax cuts and inflation

Supp.X1X2Y<- c(5,5,5) #set the means of X and Y variables

Supp.CovMatrix.X1X2Y <- matrix(c(10,sup.p12,sup.py1,

sup.p12,10,sup.py2,

sup.py1,sup.py2,10),3,3) # creates the covariate matrix

set.seed(42)

SuppData<-mvrnorm(n=100, mu=Supp.X1X2Y,Sigma=Supp.CovMatrix.X1X2Y, empirical=TRUE)

#Covert them to a "Data.Frame"

SuppData<-as.data.frame(SuppData)

colnames(SuppData) <- c("TaxCuts","inflation","growth")

###############Model 1

TaxCutsOnly<-(lm(growth~ TaxCuts, data = SuppData))

###############Model 2

Full.Model<-lm(growth~ TaxCuts+inflation, data = SuppData)stargazer(TaxCutsOnly,Full.Model,type="html",

column.labels = c("TaxCutsOnly", "Full.Model"),

intercept.bottom = FALSE,

single.row=TRUE,

star.cutoffs=c(.05,.01,.001),

notes.append = FALSE,

header=FALSE)| Dependent variable: | ||

| growth | ||

| TaxCutsOnly | Full.Model | |

| (1) | (2) | |

| Constant | 3.750*** (0.578) | 6.071*** (0.452) |

| TaxCuts | 0.250* (0.098) | 0.560*** (0.073) |

| inflation | -0.774*** (0.073) | |

| Observations | 100 | 100 |

| R2 | 0.063 | 0.565 |

| Adjusted R2 | 0.053 | 0.557 |

| Residual Std. Error | 3.077 (df = 98) | 2.106 (df = 97) |

| F Statistic | 6.533* (df = 1; 98) | 63.116*** (df = 2; 97) |

| Note: | p<0.05; p<0.01; p<0.001 | |

- You will notice tax cuts alone, 0.25, was lower than 0.5595238 controlling for inflation.

- However, you will notice inflation,-0.7738095, has a bigger effect (and negative) effect than tax cuts 0.5595238

- So in other words, yes tax cuts work but they don’t override inflation!

Lets try to graph our predictions

- Challenge is that we need to account for 2 predictors now.

- So simple scatter plots will not work

- Also how you plot depends on your theory/experiment/story

- We need to control for inflation (or view tax slope at different levels of inflation)

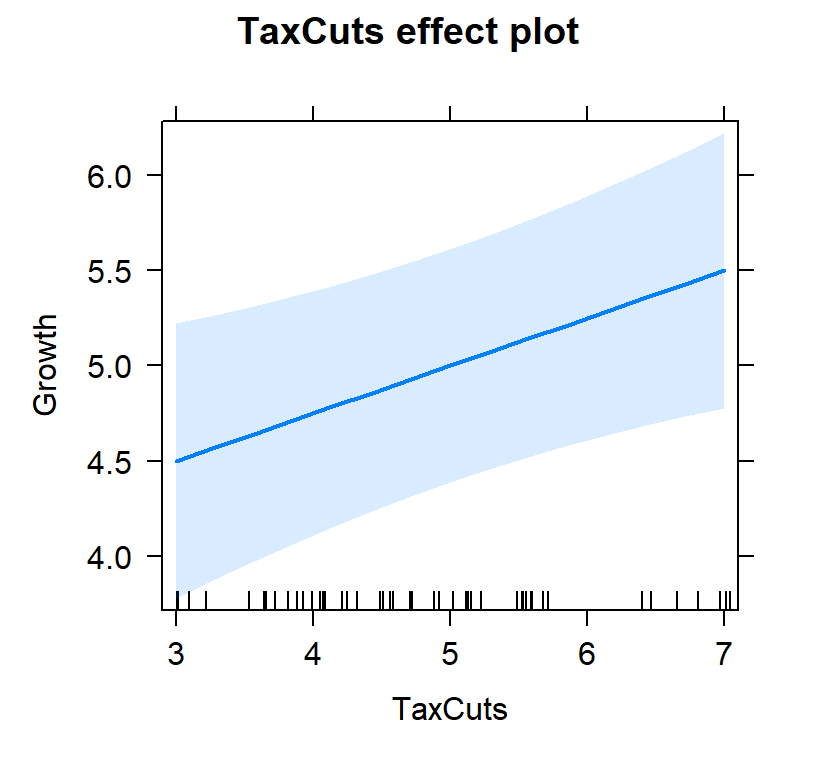

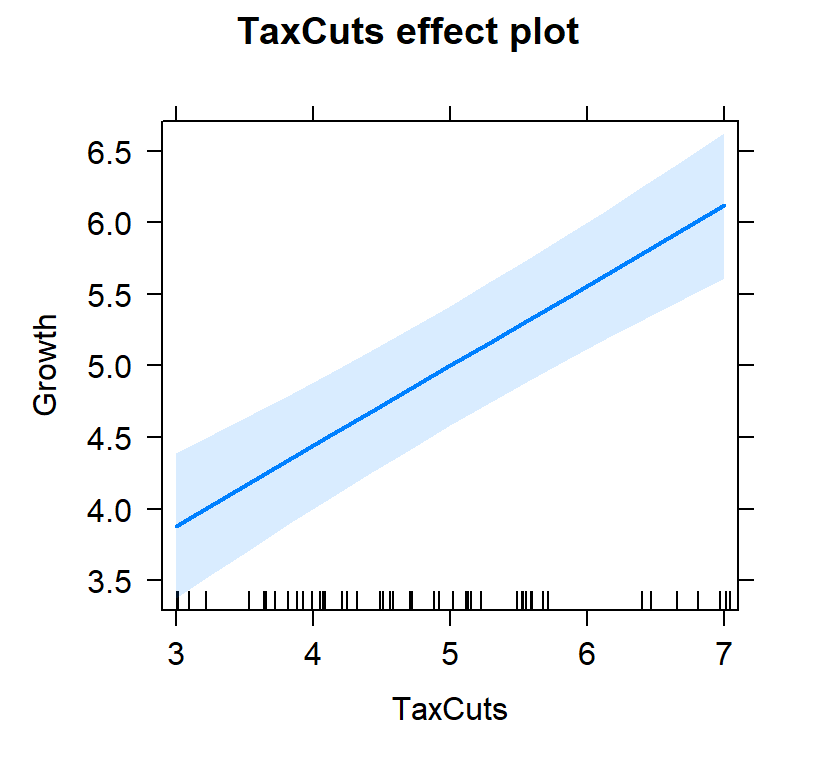

- First lets view the tax slope without controlling for inflation

#plot individual effects

Tax.Model.Plot <- allEffects(TaxCutsOnly, xlevels=list(TaxCuts=seq(3, 7, 1)))

plot(Tax.Model.Plot, 'TaxCuts', ylab="Growth")

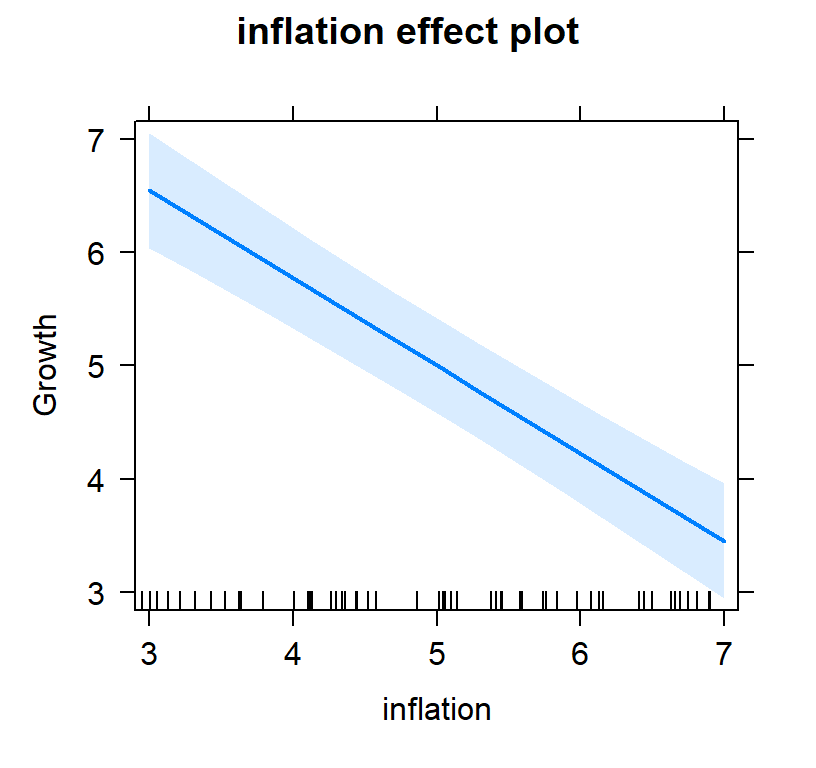

- Now lets view it controlling for inflation

#plot individual effects

Full.Model.Plot <- allEffects(Full.Model, xlevels=list(TaxCuts=seq(3, 7, 1),inflation=seq(3, 7, 1)))

plot(Full.Model.Plot, 'TaxCuts', ylab="Growth")

plot(Full.Model.Plot, 'inflation', ylab="Growth")

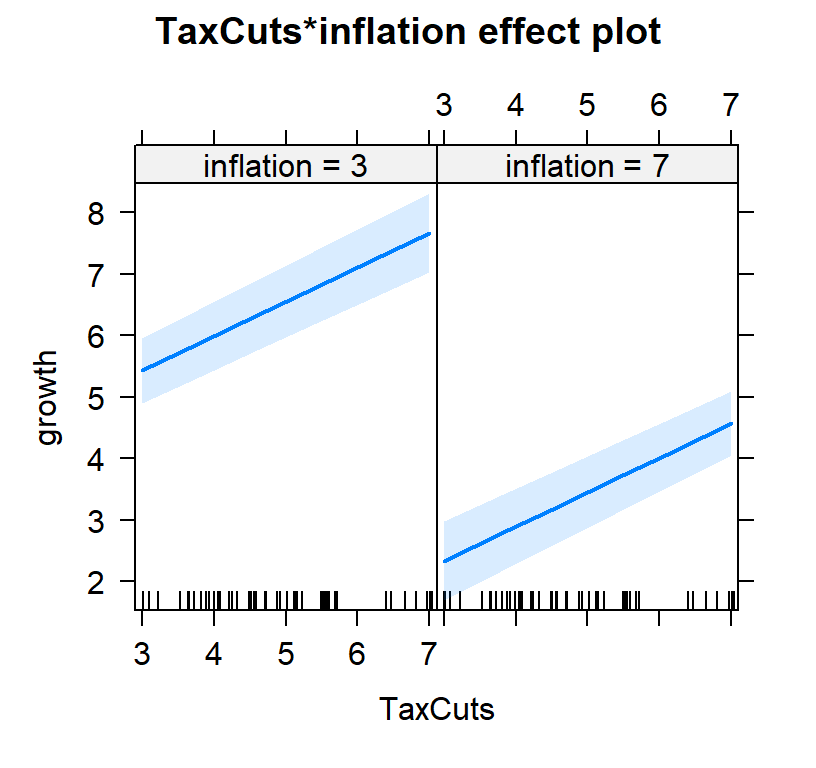

#plot both effects

Full.Model.Plot2<-Effect(c("TaxCuts", "inflation"), Full.Model,xlevels=list(TaxCuts=c(3, 7), inflation=c(3,7)))

plot(Full.Model.Plot2)

Multiple Linear Regression Assumptions

Multicollinearity: Predictors cannot be fully (or nearly fully) redundant [check the correlations between predictors]

Homoscedasticity of residuals to fitted values

Normal distribution of residuals

Absence of outliers

Ratio of cases to predictors

- Number of cases must exceed the number of predictors

- Barely acceptable minimum: 5 cases per predictor

- Preferred minimum: 20-30 cases per predictor

- This is all subject to a power analysis

Linearity of prediction

Independence (no auto-correlated errors)

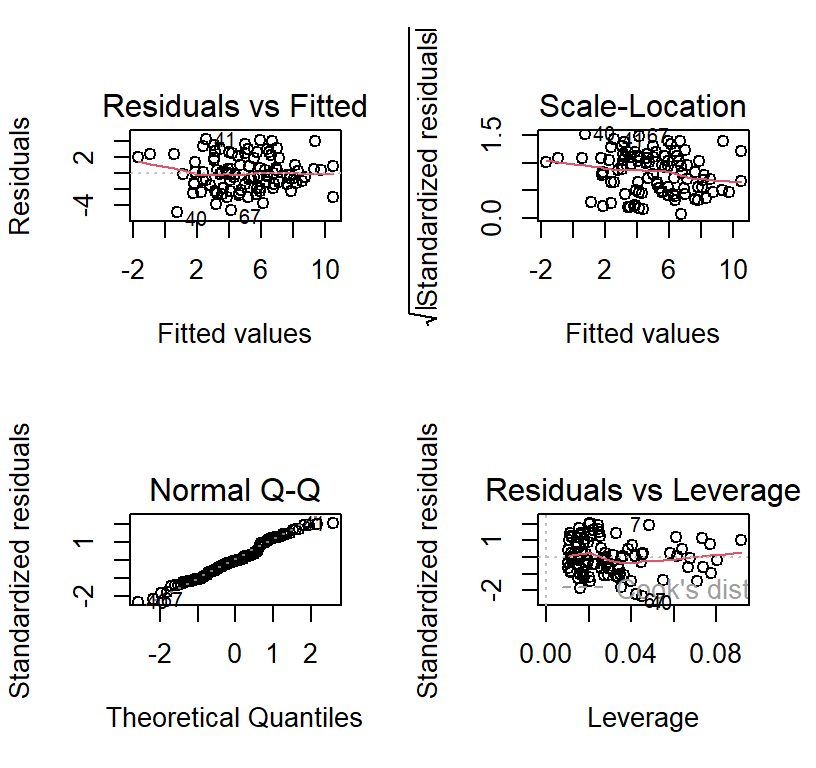

Fast and dirty method to check some of the assumptions

- Its better to just plot your data, but its fun fast check

Too see them all go to http://ademos.people.uic.edu/Chapter12.html

layout(matrix(c(1,2,3,4),2,2))

plot(Full.Model)

library(gvlma)

Full.Model.Assumptions <- gvlma(Full.Model)

summary(Full.Model.Assumptions)##

## Call:

## lm(formula = growth ~ TaxCuts + inflation, data = SuppData)

##

## Residuals:

## Min 1Q Median 3Q Max

## -4.805 -1.386 -0.138 1.677 4.202

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 6.07143 0.45203 13.431 < 2e-16 ***

## TaxCuts 0.55952 0.07303 7.662 1.39e-11 ***

## inflation -0.77381 0.07303 -10.596 < 2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 2.106 on 97 degrees of freedom

## Multiple R-squared: 0.5655, Adjusted R-squared: 0.5565

## F-statistic: 63.12 on 2 and 97 DF, p-value: < 2.2e-16

##

##

## ASSESSMENT OF THE LINEAR MODEL ASSUMPTIONS

## USING THE GLOBAL TEST ON 4 DEGREES-OF-FREEDOM:

## Level of Significance = 0.05

##

## Call:

## gvlma(x = Full.Model)

##

## Value p-value Decision

## Global Stat 2.3081 0.6793 Assumptions acceptable.

## Skewness 0.1939 0.6597 Assumptions acceptable.

## Kurtosis 1.4644 0.2262 Assumptions acceptable.

## Link Function 0.4897 0.4841 Assumptions acceptable.

## Heteroscedasticity 0.1600 0.6891 Assumptions acceptable.Interactions

- Interactions have the same meaning they did in ANOVA

- there is a synergistic effect between two variables

- However now we can examine interactions between continuous variables

- Additive Effects

\[Y = B_1X + B_2Z + B_0\]

- Interactive Effects:

\[Y = B_1X + B_2Z + B_3XZ + B_0\]

Example of Interaction

- We need to make multivariate set of variables and then force an interaction

- DV: Reading comprehension, IVs: Age + IQ

- These are not all mean centered because of interpretation

library(car)

set.seed(12345)

# 250 people

n <- 250

# Uniform distrobution of Ages (5 to 15 year olds), but 5 = 0 point

X <- runif(n, 0, 10)

# Centered normal distrobution of IQ (100 +-15)

Z <- rnorm(n, 0, 15)

e <- rnorm(n, 0, sd=10)

# Our equation to create Y

Y = .1*X + .25*Z + .1*X*Z + 50 + e

#Built our data frame

Reading.Data<-data.frame(ReadingComp=Y,Age=X,IQ=Z)Lets test an interaction

- Model 1: Examine a main-effects model (X + Z) [not necessary but useful]

- Model 2: Examine a main-effects + Interaction model (X + Z + X:Z)

- Note: You can simply code it as X*Z in r, as it will automatically do (X + Z + X:Z)

#models

Centered.Read.1<-lm(ReadingComp~Age+IQ,Reading.Data)

Centered.Read.2<-lm(ReadingComp~Age*IQ,Reading.Data)

stargazer(Centered.Read.1,Centered.Read.2,type="html",

column.labels = c("Main Effects", "Interaction"),

intercept.bottom = FALSE, single.row=TRUE,

star.cutoffs=c(.05,.01,.001), notes.append = FALSE,

header=FALSE)| Dependent variable: | ||

| ReadingComp | ||

| Main Effects | Interaction | |

| (1) | (2) | |

| Constant | 47.710*** (1.388) | 48.288*** (1.312) |

| Age | 0.546* (0.225) | 0.440* (0.213) |

| IQ | 0.817*** (0.045) | 0.333*** (0.095) |

| Age:IQ | 0.085*** (0.015) | |

| Observations | 250 | 250 |

| R2 | 0.582 | 0.630 |

| Adjusted R2 | 0.578 | 0.626 |

| Residual Std. Error | 10.266 (df = 247) | 9.670 (df = 246) |

| F Statistic | 171.653*** (df = 2; 247) | 139.732*** (df = 3; 246) |

| Note: | p<0.05; p<0.01; p<0.001 | |

- Also change in \(R^2\) is significant, as we might expect

ChangeInR<-anova(Centered.Read.1,Centered.Read.2)

ChangeInR## Analysis of Variance Table

##

## Model 1: ReadingComp ~ Age + IQ

## Model 2: ReadingComp ~ Age * IQ

## Res.Df RSS Df Sum of Sq F Pr(>F)

## 1 247 26029

## 2 246 23005 1 3024 32.336 3.665e-08 ***

## ---

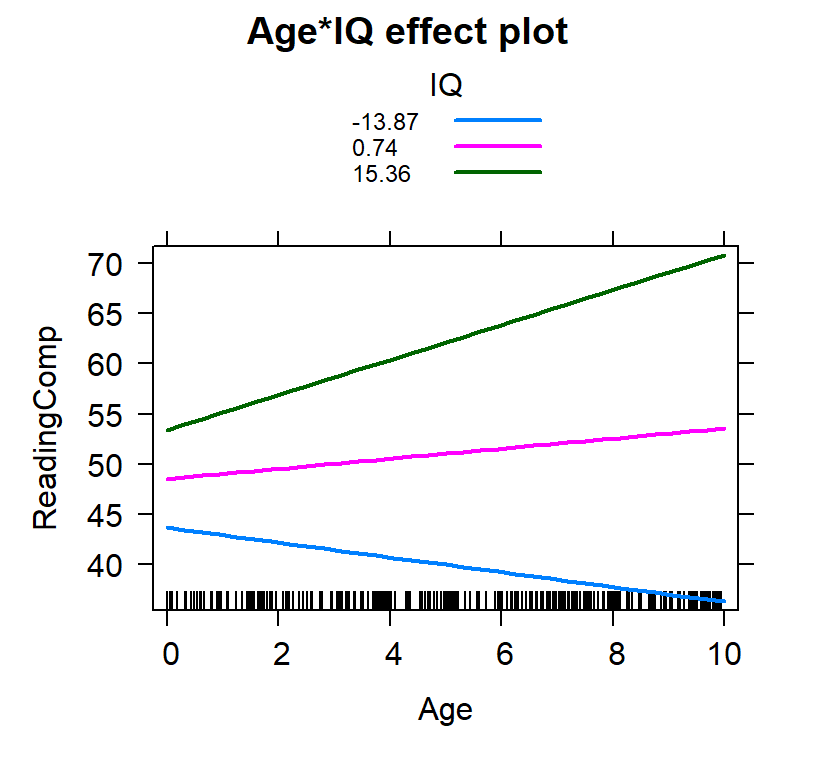

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1How visualize this?

- Well, there are some options

- We can do a fancy-pants surface plot, but that is hard to put into a paper

- More common this is to examine slope of one factor at different levels of the other (Simple Slopes)

- What we need to decide is at which levels

Based on the SD

- We select 3 values: \(M-1SD\), \(M\), \(M+1SD\)

- Not it does not have to be 1 SD, it can be 1.5,2 or 3

- Assumes normality for IV

IQ.SD<-c(mean(Reading.Data$IQ)-sd(Reading.Data$IQ),

mean(Reading.Data$IQ),

mean(Reading.Data$IQ)+sd(Reading.Data$IQ))

IQ.SD<-round(IQ.SD,2)

IQ.SD## [1] -13.87 0.74 15.36Inter.1c<-effect(c("Age*IQ"), Centered.Read.2,

xlevels=list(Age=seq(0,10, 1),

IQ=IQ.SD))

plot(Inter.1c, multiline = TRUE)